Songwe Hill

Project Highlights

- Location: Malawi, Africa

- Advanced stage rare earth project

- 2019 resource update – 60% increase in Measured & Indicated Resources

- 2022 Definitive Feasibility Study completed

- Malawi – stable jurisdiction with major infrastructure developments

- Sustainable development and CSR – integral to Mkango’s vision

- Supportive government

Mkango Mine Development Project – Songwe Hill

The Songwe Hill project is located in a stable jurisdiction with major infrastructure already in place. The project is approximately 70km from the former capital Zomba and approximately 90km from the commercial centre of Blantyre, which has an international airport and a railhead. Paved roads run from the urban centres to within 12km of Songwe Hill. Secondary gravel and dirt roads provide vehicle access to the exploration camp, with recently upgraded bridges capable of taking 20-tonne trucks.

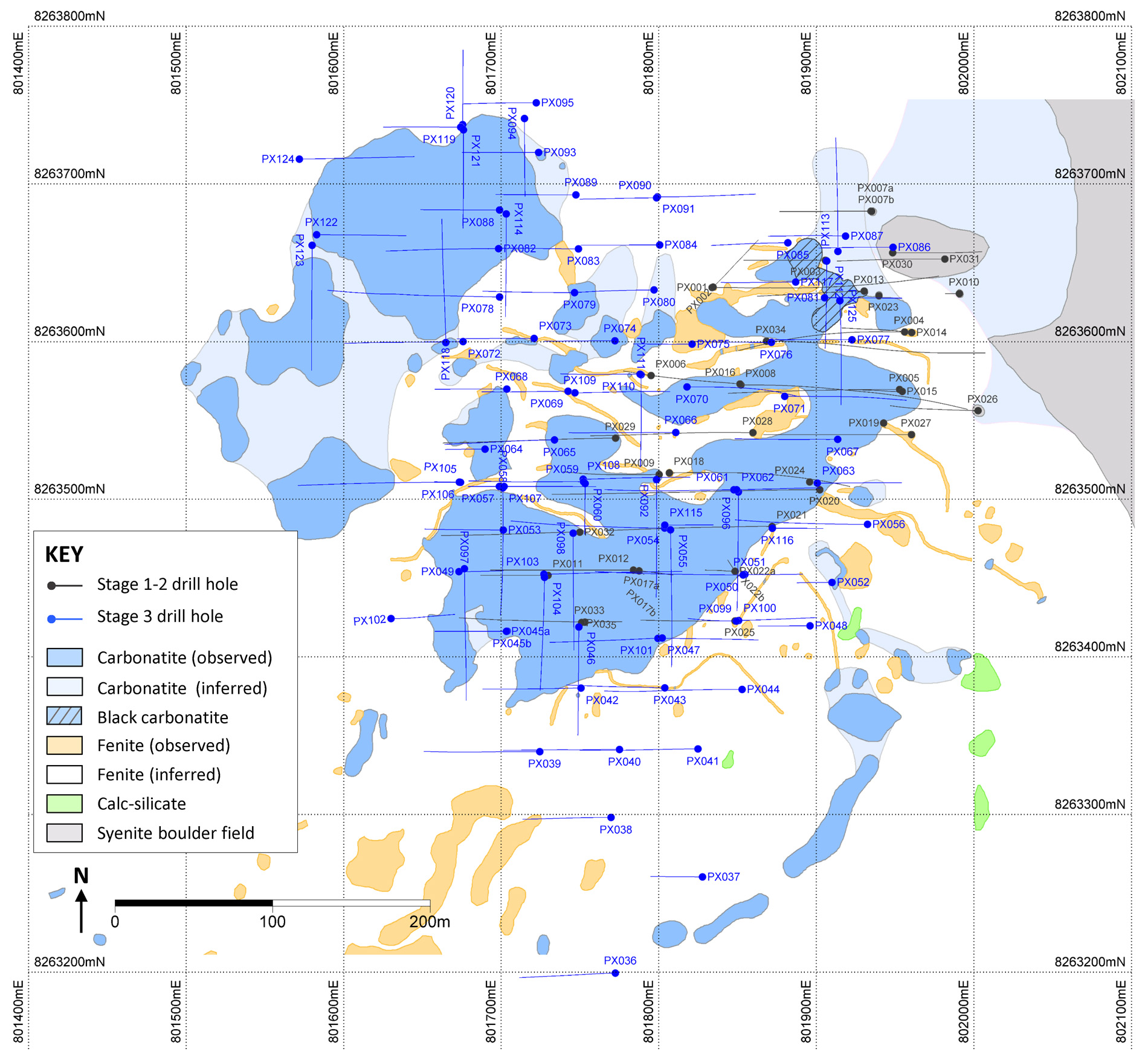

Songwe Hill Rare Earths Deposit

- Carbonatite hosted rare earth mineralisation

- Updated resource estimate announced February 2019

- 60% increase in Measured & Indicated Resources

- 95% of Measured & Indicated Resources <160m from surface – majority accessible by open pit mining

- Broad mineralised zones as opposed to dykes or veins

- Synchysite dominated rare earth mineralogy

{kind=link}

{kind=link}

Mkango Refinery Development Project - Pulawy Separation Plant

On June 7, 2021, Mkango announced that Mkango and Grupa Azoty Zakłady Azotowe ”Pulawy” S.A. (“Grupa Azoty PULAWY”) have agreed to work together towards development of a rare earth separation plant in Poland.

A new Polish wholly owned subsidiary of Mkango, Mkango Polska, has been established and a highly experienced Country Director for Poland, Dr Jarosław Pączek, has been appointed, together with rare earth separation experts, Carester, and a strong team of technical advisors and engineers.

Grupa Azoty PULAWY (Warsaw Stock Exchange: ZAP) is part of The Grupa Azoty Group, the European Union’s second largest manufacturer of nitrogen and compound fertilizers, and a major chemicals producer. Its products are exported to over 20 countries around the world, including Europe, the Americas and Asia.

Development of the Plant is expected to bring significant benefits to the Mkango group:

- Higher value-added products with increased margins – targeting 2,000 tonnes per year of separated neodymium (Nd) / praseodymium (Pr) oxides, and 50 tonnes per year dysprosium (Dy) and terbium (Tb) oxides in a heavy rare earth enriched carbonate

- Greater integration – plant development fully underpinned by sustainably sourced, purified mixed rare earth carbonate from Mkango’s Songwe Hill operations, with other synergies being evaluated

- Increased marketing flexibility with a broader range of potential customers – future opportunities to produce and market separated heavy rare earths

- Catalyst for regional growth and the green transition – potential for further downstream developments and related businesses, including renewables, creating additional jobs in the region

Feasibility studies for the Plant have been undertaken in parallel with Mkango’s Songwe Hill rare earths project in Malawi and other opportunities, including Mkango’s interest in HyProMag Limited, which is developing production of short loop recycled rare earth magnets in the UK.

Mkango Rare Earth Magnet Recycling

Through its ownership of Maginito Limited (www.maginito.com), Mkango is also developing green technology opportunities in the rare earths supply chain, encompassing neodymium (NdFeB) magnet recycling as well as innovative rare earth alloy, magnet and separation technologies. Maginito holds a 100% interest in UK rare earth (NdFeB) magnet recycler, HyProMag Limited (www.hypromag.com).

Mkango Exploration Projects

Thambani U-Ta-Nb project

- Licence area of 98km2 in Mwanza and Chikwawa districts in southwestern Malawi

- Uranium, tantalum and niobium hosted in nepheline syenite gneiss and associated veins

- Potential for U-Ta-Nb mineralisation along a strike length of >3km revealed by airborne and ground radiometric surveys and surface sampling

- Tete–Nacala railway traverses the licence

Mkango Milestones

-

2011

Listed on TSX-V exchange.

-

2012

Maiden Indicated and Inferred Mineral Resource estimate at Songwe Hill.

-

2016

Listed on London AIM exchange.

-

2017

Agreement with Talaxis to fund development of Songwe Hill and commercialisation of new magnet technologies.

-

2018

£6 Million (C$10.5 Million) Talaxis investment for Songwe Hill Feasibility Study.

-

2019

60% increase in Measured and Indicated Resources at Songwe Hill.

-

2022

Definitive Feasibility Study completed for Songwe Hill.